Thoroughly understanding your business’ financial performance is critical

for success in today’s increasingly competitive agricultural environment.

Accurate records and financial statements are the foundation material

required to analyze the financial condition and trends of your operation.

All agricultural businesses, from small part-time farms to large commercial

operations, require financial statements completed on a regular basis to

track financial progress including equity, liquidity, income, and cash flow.

How do financial statements prove useful?

As a tool for management

Successful managers use financial statements in combination with production

records to identify strengths and weaknesses in their operation. In addition to

tracking trends in assets and liabilities, financial statements can reveal where

revenues are originating and where expenses are occurring. Financial statements

can be used to time cash expenditures and plan for credit needs. Finally, these

statements provide the critical data for ratio analysis and benchmarking.

Preparing Agricultural

Financial Statements

2

As a tool for use with lenders and

other professionals

Lenders request, and in most cases require,

an accurate set of financial statements to

accompany a credit request. A carefully

prepared set of financial statements shows

you have a detailed understanding of your

business and its repayment capacity. Others,

such as attorneys and financial planners,

also need financial statements for services

such as estate and retirement planning,

organizational establishment, and buy-sell

agreements for business transition purposes.

As a tool for tax compliance

A carefully prepared set of financial

statements can make life much easier when

tax time comes around.

This prevents last minute information

collection and provides peace of mind

in an IRS audit. Financial statements can

be prepared by individuals, in-house

employees or accountants. Statements

prepared by accountants will range from

simply compiling a business owner’s

numbers, to reviewing and reconciling

numbers, to a formal, unqualified audit.

Even if you have an accountant that keeps

your operation’s books and prepares your

taxes, it’s still important to understand

how financial statements are prepared.

Although accountants are professionals

and are knowledgeable in their field, no one

understands your business like you do.

Financial statements include the balance

sheet, income statement, statement of

owner equity, statement of cash flows, and

cash flow projection. Our discussion will

focus on the three most commonly used

financial statements: the balance sheet,

income statement and cash flow projection.

Financial statements are interrelated;

therefore, proper timing of the statements is

important to gain the most benefit.

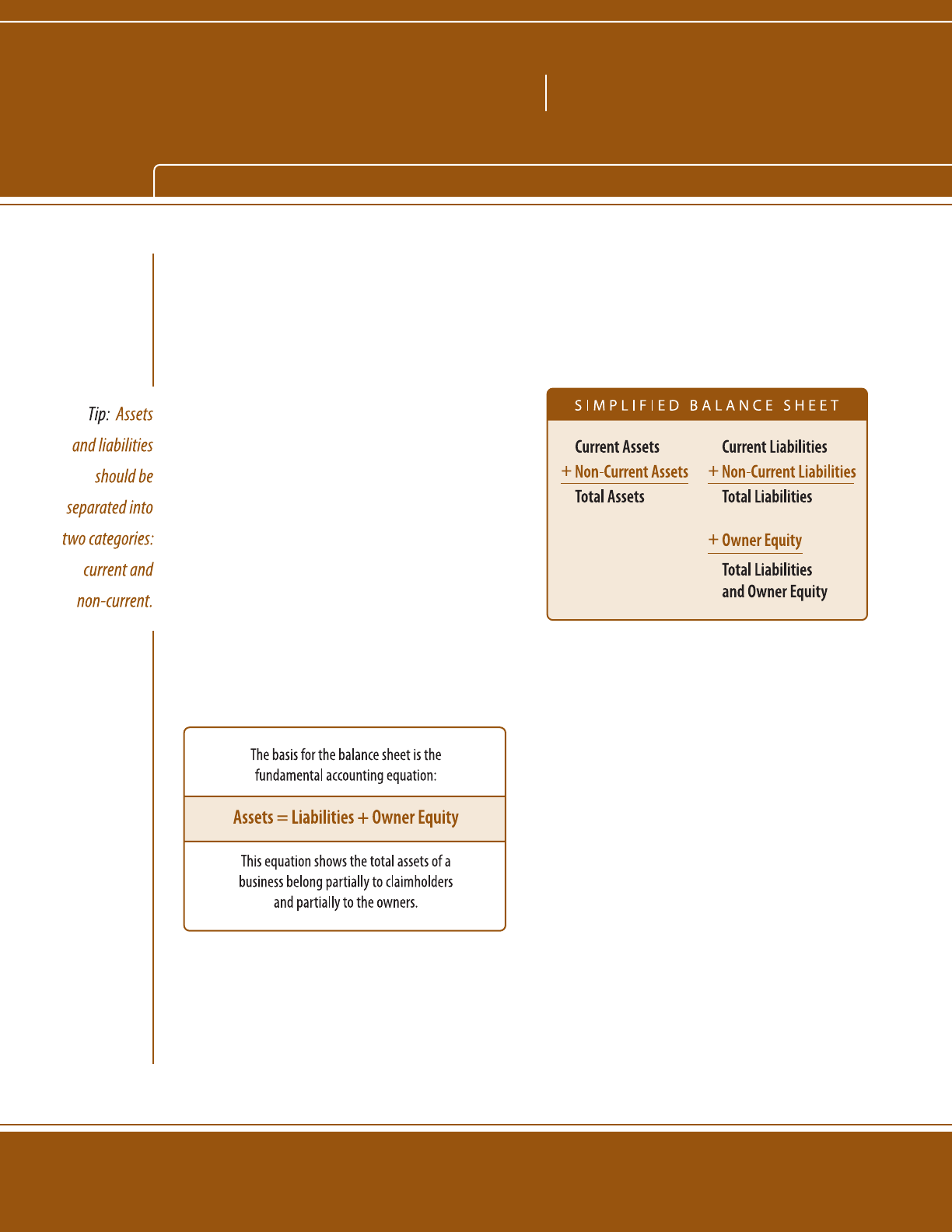

Balance sheet

The balance sheet is a statement of financial

position at a specific point in time or a

financial snapshot of the business. The balance

sheet reflects the result of all past transactions

but not how the current financial position was

obtained. The balance sheet consists of three

main parts:

Assets

Assets include anything that is owned by

the entity that has monetary value. Standard

accounting practices value assets at either

cost, market value or the lower of the cost or

market, depending on what is preferred by the

person preparing or requesting the balance

© 2008 Northwest Farm Credit Services, Spokane, WA. All Rights Reserved. Reproduced with permission only.

sheet. Assets valued on a cost basis are listed

at the historical cost less any accumulated

depreciation. Market valued assets are listed

at fair market value based on the asset’s

condition, location or other relevant factors.

Assets valued at the lower of cost or market

are assigned either the cost value or the

market value, whichever is lower. Assets should

be separated into two categories: current and

non-current. A more detailed discussion of

asset classification will follow.

Liabilities

Liabilities include all claims against the

business by creditors, suppliers or any other

person or institution to which a debt is

owed. Liabilities, like assets, are classified

into current and non-current categories.

Owner equity

Owner equity, or net worth, is the difference

between total assets and total liabilities. It

reflects the owner’s stake in the business

and includes investment capital and

retained profits. In a corporate business

structure, owner equity will include

stockholder’s equity, additional paid-in

capital and retained earnings.

Assets

Current Assets

Current assets are the first classification of

assets appearing on the balance sheet. Current

assets include items such as cash or assets

that can and will be turned into cash within

a year without disrupting normal business

operations. Current assets also include any

items that will be consumed within a year.

Examples of current assets include:

•

Cash - Any cash on hand in checking or

savings accounts.

•

Marketable securities - Stock or other

securities that are publicly traded and

3

Preparing Agricultural

Financial Statements

BUSINESS TOOLS

4

can be easily turned to cash. This would

include only those securities which the

owner intends to convert to cash within

the year. Stock or other securities held for

long-term investment or for retirement

should be considered non-current assets.

•

Accounts receivable - Any amounts

owed to the business for products or

services provided for which payment has

not been received.

•

Marketable inventories - Crops and

livestock held for sale. Do not include

breeding livestock, as they are considered

non-current assets.

•

Cash investment in growing crops -

The dollar amount of inputs invested in

growing crops after planting but before

harvest.

•

Supplies - Any items such as fertilizer,

chemicals or feed that are on hand and

scheduled to be used in the next year.

•

Prepaid expenses - Items that have

been paid for but not yet consumed in full

(examples include insurance premiums,

rent or lease payments, and certain taxes).

Non-current assets

The second classification of assets is

non-current assets. These assets support

production activities and are considered

to have a life greater than one year. In

agriculture, common non-current assets

include machinery and equipment. Breeding

livestock are classified as non-current assets.

If a personal balance sheet is prepared,

non-current personal assets may be

included, such as household furnishings

and equipment, personal and recreational

vehicles, and personal retirement accounts.

Another major category of non-current

assets is real estate, including land, buildings

and improvements. A personal residence

may also be included, if the balance sheet is

prepared for a consolidated entity.

Liabilities

Similar to assets, liabilities are also classified

as either current or non-current. The liability

section of the balance sheet should include

all obligations (classified based on repayment

schedule) as of the date of the balance sheet.

Current liabilities

Current liabilities include all debts and

obligations that are due within the next 12

months. Examples of some common current

liabilities are:

•

Accounts Payable - Money owed to

BUSINESS TOOLS

suppliers or other businesses for products

or services your business has received but

not yet made payment for.

•

Operating loans - Any outstanding

balances on revolving or non-revolving

operating lines of credit.

•

Principal portion of term loans due

within the next year - The total amount

of principal on term loans that is due to

be paid within the year.

•

Accrued interest - The amount of

interest that has accrued on all loans. This

is the total amount of interest that would

be due if all loans were paid off as of the

day of the balance sheet – it is not the

total amount of interest due to be paid in

the next 12 months.

•

Accrued income and property taxes

- Property taxes are typically paid in a

period following when they are incurred,

and income taxes are paid as frequent as

every quarter, so the balance sheet will

often reflect some accrued tax liability.

•

Other accrued expenses - Items such as

rents and leases that have been utilized but

not yet paid would be accrued expenses.

•

Credit card debt - Credit card debt,

including principal and interest, is

included as a current liability. It’s common

in agriculture for loans to be financed

for one year with the option of renewal

at the end of the year given acceptable

repayment performance. If the lender is

under no obligation to renew the loan

at the end of the original agreement, the

liability should be classified as a current

liability. This treatment may distort

financial ratios, but legally the entire

obligation is due at the end of one year.

Non-current liabilities

Non-current liabilities capture all obligations

that are due and payable beyond one year.

The most common non-current liabilities

are term loans used to finance machinery,

equipment, breeding livestock, or real estate.

The portion of the term loan due beyond 12

months is considered a non-current liability.

Remember the principal amount due within

12 months is a current liability.

Contingent liabilities

Another category of liabilities is contingent

liabilities, which includes such items as

guarantees, pending lawsuits, and federal

and state tax disputes. These items appear

as footnotes to the balance sheet and

are not liabilities at the present, but the

potential for an obligation exists.

5

Preparing Agricultural

Financial Statements

6

Owner Equity

Owner equity is a residual amount after

liabilities are subtracted from assets (see

Exhibit 1 below and Exhibit 2 on the next

page). Owner equity reflects the owner’s

investment of capital into the business and

retained earnings which are generated over

time. Retained earnings are profits that have

been reinvested back into the business rather

than withdrawn by the owners or paid out in

dividends in the case of a corporation.

Balance sheet considerations

The ownership structure of agricultural

businesses is becoming increasingly

complex. The traditional sole proprietorship

is no longer the norm in agriculture.

Combinations of partnerships, corporations,

and limited liability companies are quickly

7

BUSINESS TOOLS

Preparing Agricultural

Financial Statements

8

emerging with one entity holding operating

assets and another entity controlling the

capital assets. It is essential to identify the

entity for which the balance sheet is being

prepared, such as business, personal or a

consolidation of both.

Timing

For analysis purposes, the timing of the

balance sheet is important. Balance sheets

are most useful when they consistently

coincide with the timing of the income

statement, usually at fiscal year-end, which

is typically the end of the income period.

The accrual adjusted income statement

(discussed later) combines other data,

including changes in the beginning and

end-of-year balance sheets.

Asset valuation

A balance sheet is only as valuable as the

quality of the information used to prepare

it. When valuing assets on a market basis, a

conservative approach is preferred, based

upon appraisals and recent sales data in

the market. When preparing a balance

sheet, it’s important to distinguish between

possession and ownership of assets. If a

partial interest in property is owned, then

only that portion should be reflected as an

asset on the balance sheet. Ownership issues

also arise in the case of “life estates” and

lease agreements.

When crop and livestock inventories are

included on the balance sheet, they should

be accompanied by a schedule detailing the

amount and value of each item, indicating

how the total value was derived.

Often a person is involved in more than

one business venture. If so, information

about assets and liabilities associated with

other businesses should be identified. One

business may show significant equity while

another is heavily leveraged. Lenders are

likely to request a consolidated balance

sheet that combines all business and

personal assets and liabilities.

Valuing leases

Numerous valuation issues arise when

preparing balance sheets which exceed

the scope of this discussion. An issue is

that of capital leases for items such as

tractors, combines, irrigation equipment,

and storage structures. In the past, many

lease obligations were simply included as

footnotes to the balance sheet. However,

these types of leases should be included on

the balance sheet.

There are two types of leases: operating

leases and capital leases. Operating leases

allow the lessee the right to use an asset for

a relatively short period of time. Operating

leases should appear as a note to the

balance sheet (unless prepaid or past due),

similar to the rental of farm land. A capital

lease is a direct substitute for purchase of

the asset with borrowed money. It transfers

substantially all the benefits and risks

inherent in the ownership of the property to

the lessee. To be considered a capital lease,

the agreement must meet any one of the

following tests:

•

The lease transfers ownership of property

to the lessee at the end of the term.

•

The lease contains a bargain purchase

option.

•

The term of the lease is at least 75 percent

of the estimated economic life of the

property.

•

The present value of the minimum lease

payment equals or exceeds 90 percent

of the fair market value of the leased

property.

Exhibit 3 below, illustrates an example of

a five-year capital lease agreement with

annual payments (due at the beginning of

the period) of $11,991. The lease is treated

similar to an equal payment, amortized loan

and must be reflected as both an asset and

a liability on the balance sheet. Although

there is no interest rate stated in the

agreement, an $11,991 annual payment for

five years at an “imputed interest rate” of 10

percent results in a present value of $50,000.

This is the initial lease value (both asset and

liability). Remember, it’s the lease investment

which is being put on the balance sheet, not

9

BUSINESS TOOLS

Preparing Agricultural

Financial Statements

10

the asset being leased.

Also in Exhibit 3, the asset is listed as a non-

current asset each year. The principal due

within the year and any accrued interest as

of the date of the statement are listed as

current liabilities, and the remaining lease

obligation is a non-current liability.

Deferred taxes

As discussed earlier, assets can be valued

on the balance sheet, either on a cost or

market value basis. A market value balance

sheet reflects the impact of deferred tax

liabilities (refer back to Exhibits 1 and 2 on

pages 6 and 7). Deferred taxes are the federal

and state taxes that would be incurred

if the business was liquidated. Deferred

taxes on current assets arise because many

agricultural producers report income on a

cash rather than accrual basis for income

tax purposes. Therefore, they do not pay

taxes on the accumulation of crop and

livestock inventories over time. Income taxes

would be due if inventories were sold and

if the expenses associated with them had

previously been deducted as cash expenses.

Deferred taxes may also be present on non-

current assets. Two examples of deferred tax

situations are:

•

Market value of assets exceeds cost less

accumulated depreciation.

•

Sales price of purchased breeding

livestock exceeds the original cost.

Income statement

A business income statement, also called a

profit and loss statement, is used to measure

revenues and expenses over an accounting

period. Unlike the balance sheet, which

reflects the financial position at any given

point in time, the income statement shows

income and expenses for a period of time,

usually one year. Income statements can be

used to determine income tax payments,

analyze a business’ expansion potential,

evaluate the profitability of an enterprise, and

assist in loan repayment analysis.

Identify entity

Identifying the business entity is also

important when preparing an income

statement. The income statement

should be prepared for the same entity

as the balance sheet, either business,

personal or consolidated. Because of the

interrelationship between the balance sheet

and income statement, the time period

covered by the income statement should be

the time between the beginning and ending

balance sheets. The most common period

is annually, although quarterly or monthly

statements are sometimes desired.

Revenues and expenses

All income statements include two

categories: revenues and expenses. However,

income statements can be prepared two

ways, depending on how revenues and

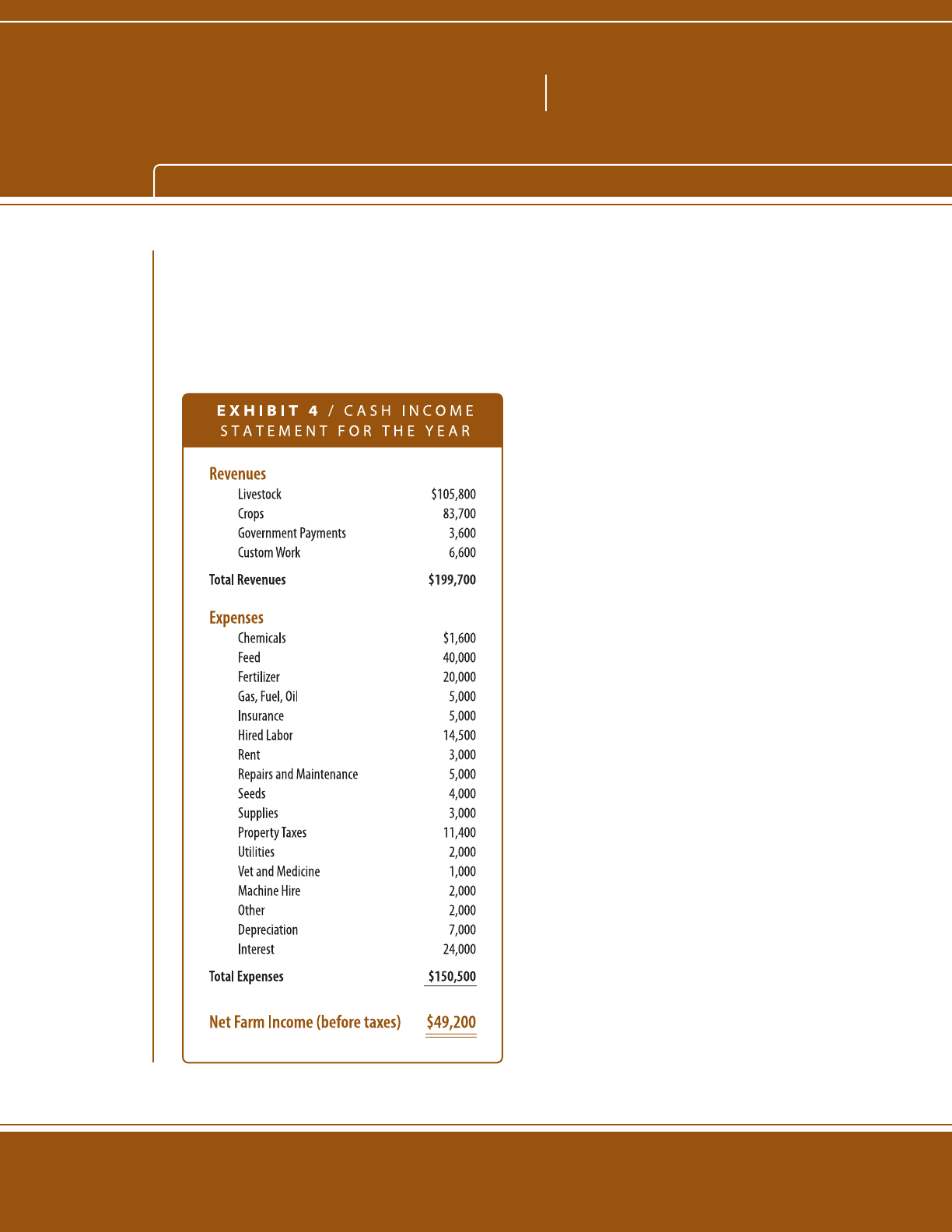

expenses are derived. A cash income

statement measures revenues only when

received and expenses only when paid.

An accrual income statement measures

revenues when generated and expenses

when incurred, whether or not cash actually

changes hands. The cash income statement

(illustrated in Exhibit 4) is the easiest to

prepare but is inadequate for measuring

true profitability because it fails to match

the timing of income and expenses.

Depreciation

Depreciation, although not a cash expense,

is included on both the cash and accrual

income statements as a way of spreading

the cost of capital purchases over their

useful life. Accelerated depreciation is

frequently used for tax purposes. If this is

the case, it should be noted accelerated

depreciation is being used, because it could

distort profitability.

Schedule F

The Schedule F tax form is often used as an

income statement. Although the Schedule

F can offer some valuable insight, it is not

an income statement and should not be

used as such. However, in some cases it can

be used effectively if three to five years of

information is provided and the business is

in a stable operating mode with no major

adjustments. Using a series of Schedule Fs

11

BUSINESS TOOLS

Preparing Agricultural

Financial Statements

12

as an income tax statement rests on the

assumption shifting income and expenses

will even out over the years.

Accrual-adjusted statements

The Farm Financial Standards Council

recommends the use of an accrual-adjusted

income statement. Ideally, a business’

accounting records will produce an accrual

statement; however, in practice, adjustments

are made to the cash income statement

(or Schedule F) to gain an accrual-adjusted

income statement. Exhibit 5 above

illustrates how accrual adjustments are

made. To convert cash income to accrual-

adjusted income, we must look at changes

between the beginning-of-year and end-

of year balance sheets. Adjustments to

revenue include changes in inventories

and accounts receivable. In the expense

section, adjustments are made for changes

in unused assets, prepaid expenses, accrued

expenses, and accounts payable. Gains or

losses on the sale of capital assets are also

added or subtracted.

Revenues and expenses can come from a

variety of sources in an agricultural business.

Categories of revenues that are usually

included in an income statement are:

•

Realized cash revenues from the sale of

agricultural commodities.

•

Unrealized income from changes in the

quantity or value of crop and livestock

inventories.

•

Realized capital gains from the sale of

capital assets.

•

Income from custom work and

government payments.

Expense items included on the income

statement vary with the type of business

but include all operating expenses, interest

and depreciation.

Cash flow projection

The balance sheet and income statement

provide present and historical financial

information that reflect past financial

performance of a business. However,

producers and lenders are often equally, if not

more, interested in future performance. For this

reason, a cash flow projection is a valuable

financial tool.

A cash flow projection summarizes cash

inflows and outflows over a given period. A

projection can be prepared for the business,

individual or a consolidation of both, similar

to the balance sheet and income statement.

The cash flow projection can be useful for

preparing projected income statements and

balance sheets and for determining:

•

The need for operating lines of credit to

cover cash flow deficits.

•

Periods of excess cash when funds could

be placed in income-earning assets such

as money markets or the Future Payment

Fund offered by Northwest Farm Credit

Services.

•

The need for changes in marketing or

expenditure plans.

•

The cash flow feasibility of a new

investment.

13

BUSINESS TOOLS

Preparing Agricultural

Financial Statements

14

•

The cash flow in a transition year before

the operation is fully engaged.

Components

While cash flow statement formats can vary,

there are three basic components: cash

inflows, cash outflows and operating finance

activities.

Exhibit 6 on the next page illustrates a

cash flow projection. Cash inflows include

receipts from farm and nonfarm activities

that are divided into relevant categories for

the type of business being examined. Cash

outflows include a detailed listing of cash

expenses as well as principal and interest

payments on term debt.

Note depreciation does not appear on the

cash flow projection because it’s not a cash

expense and will not impact cash flow. The

operating finance activities section outlines

the net cash flows for each quarter along

with the short-term borrowing needs,

interest accrued and repayment of the line

of credit.

Different scenarios

A one-year projection can be completed for

different scenarios to examine price, cost

and related impacts.

Cash flow projections for multiple years may

also be useful when development is being

done, in order to project cash needs prior to

full production or adequate production to

break even.

Different cash flow scenarios may include:

“How would cash flow be affected if

commodity prices were 50 cents lower

than expected?” or “What is the impact of

a 10 percent increase in fertilizer costs?”

Testing these options helps identify

how sensitive an operation or projected

scenario is to changes in the market

environment. It’s important to remember

a cash flow projection is only as good as

the assumptions and information used to

prepare it.

15

BUSINESS TOOLS

Preparing Agricultural

Financial Statements

Whether you are preparing your own

statements, or analyzing those prepared

by an accountant, this publication should

provide a good basic understanding

of how to prepare financial statements

that are valuable both internally as a

management tool, and externally for use

with outside professionals.

farm-credit.com

1.800.743.2125