Confidential Financial Disclosure Guide, Table of Contents 2

Version: 1/2019

Table of Contents

Table of Contents ...................................................................................................................... 2

Introduction ............................................................................................................................... 5

Objectives ............................................................................................................................. 5

Contents ................................................................................................................................ 5

Disclaimer ............................................................................................................................. 5

Section 1: Confidential Financial Disclosure System .............................................................. 6

Purpose .................................................................................................................................. 6

Authority ............................................................................................................................... 6

Officials Required to File ...................................................................................................... 6

Types of Reports and Filing Deadlines ................................................................................. 9

Confidential Financial Disclosure Forms ........................................................................... 14

Extensions ........................................................................................................................... 15

Filing Penalties.................................................................................................................... 16

Agency Procedures ............................................................................................................. 16

Records Management.......................................................................................................... 16

Section 2: OGE Form 450 – Report Contents ....................................................................... 18

Summary of Contents ......................................................................................................... 18

Reporting Periods and Individuals Covered ....................................................................... 18

Spouses and Dependent Children ....................................................................................... 19

Use of Brokerage Statements and Attachments .................................................................. 21

Cover Page .......................................................................................................................... 21

Part I: Assets and Income ................................................................................................... 24

Part II: Liabilities ................................................................................................................ 33

Part III: Outside Positions ................................................................................................... 35

Part IV: Agreements or Arrangements ............................................................................... 36

Part V: Gifts and Travel Reimbursements (Annual Filers Only) ....................................... 38

Section 3: Review Procedures ............................................................................................... 42

Basic Steps .......................................................................................................................... 42

Certification Requirements ................................................................................................. 42

Review Timeframes ............................................................................................................ 44

Tools of Review .................................................................................................................. 45

When to Obtain Additional Information ............................................................................. 46

Reviewer Notes and Annotations........................................................................................ 47

Section 4: Reviewing Specific Types of Entries.................................................................... 49

401(k) Plan .......................................................................................................................... 49

403(b) Plan .......................................................................................................................... 49

457 Plan .............................................................................................................................. 50

American Depositary Receipt (ADR) ................................................................................. 50

Annuity (fixed).................................................................................................................... 51

Annuity (variable) ............................................................................................................... 51

Award or Prize .................................................................................................................... 52

Bond (corporate) ................................................................................................................. 52

Bond (municipal) ................................................................................................................ 53

Bonus (cash)........................................................................................................................ 54

Superseded

Confidential Financial Disclosure Guide, Table of Contents 3

Version: 1/2019

Brokerage Account ............................................................................................................. 55

Carried Interest.................................................................................................................... 55

Cash Account ...................................................................................................................... 57

Cash Balance Pension Plan ................................................................................................. 57

Collectible Item ................................................................................................................... 57

College Savings Plan (529 plan) ......................................................................................... 58

Common Trust Fund of a Bank .......................................................................................... 59

Contingency Fee ................................................................................................................. 59

Deferred Compensation ...................................................................................................... 60

Defined Benefit Plan ........................................................................................................... 63

Defined Contribution Plan .................................................................................................. 64

Director Fee ........................................................................................................................ 65

Employee Stock Ownership Plan........................................................................................ 66

Employee Stock Purchase Plan ........................................................................................... 67

Equity Index-Linked Note .................................................................................................. 68

Exchange-Traded Fund ....................................................................................................... 69

Executor or Administrator Fee............................................................................................ 69

Farm (operated as a business) ............................................................................................. 70

Farm or Farmland (passive interest) ................................................................................... 71

Foreign Exchange Position (“forex”) .................................................................................. 72

Futures Contract (“future”) ................................................................................................. 73

Gambling Winnings ............................................................................................................ 73

Government Agency or GSE Security ................................................................................ 74

Government Benefit or Payment ........................................................................................ 75

Honorarium ......................................................................................................................... 76

Intellectual Property ............................................................................................................ 77

Investment Fund (general) .................................................................................................. 77

IRA, Roth IRA, SEP IRA, or Keogh Plan .......................................................................... 79

Law Firm (partnership) ....................................................................................................... 81

Legal Practice (solo practice).............................................................................................. 82

Life Insurance (term) .......................................................................................................... 83

Life Insurance (variable) ..................................................................................................... 83

Life Insurance (whole or universal) .................................................................................... 84

Loan Made to Another Party ............................................................................................... 85

Managed Account ............................................................................................................... 85

Margin Account .................................................................................................................. 86

Money Market Fund ........................................................................................................... 87

Money Purchase Pension Plan ............................................................................................ 87

Mutual Fund ........................................................................................................................ 87

Oil, Gas, or Other Mineral Rights Lease ............................................................................ 89

Option (incentive stock option plan)................................................................................... 89

Option (put or call purchased) ............................................................................................ 90

Option (put or call written) ................................................................................................. 92

Phantom Stock .................................................................................................................... 93

Precious Metal .................................................................................................................... 95

Prepaid Tuition Plan (529 plan) .......................................................................................... 95

Superseded

Confidential Financial Disclosure Guide, Table of Contents 4

Version: 1/2019

Real Estate .......................................................................................................................... 96

Real Estate Holding Company ............................................................................................ 97

Restricted Stock .................................................................................................................. 99

Restricted Stock Unit (RSU) ............................................................................................. 100

Salary ................................................................................................................................ 101

Self-Funded Defined Benefit Plan .................................................................................... 101

Severance Payment (cash) ................................................................................................ 102

Short Sale .......................................................................................................................... 103

Small Business (operated as a business) ........................................................................... 104

Small Business (passive interest) ...................................................................................... 106

Stable Value Fund ............................................................................................................. 106

Stock ................................................................................................................................. 107

Stock Appreciation Right .................................................................................................. 108

Third-Party Escrow Agreement ........................................................................................ 109

TIAA ................................................................................................................................. 111

Treasury Security .............................................................................................................. 112

Trust (irrevocable) ............................................................................................................ 112

Trust (revocable living)..................................................................................................... 114

Trustee Fee ........................................................................................................................ 115

UGMA or UTMA Account ............................................................................................... 116

Unit Investment Trust ....................................................................................................... 117

Virtual Currency ............................................................................................................... 118

Will or Estate .................................................................................................................... 118

Superseded

Confidential Financial Disclosure Guide, Introduction 5

Version: 1/2019

Introduction

This guide was produced by the U.S. Office of Government Ethics (OGE) as a

reference manual for use by reviewers of the OGE Form 450 (Executive Branch

Confidential Financial Disclosure Report).

Objectives

In this guide, you will learn:

• the key elements of the executive branch confidential financial disclosure system;

• what a filer must disclose in the OGE Form 450; and

• how to analyze entries for technical sufficiency.

Contents

The guide contains four sections:

• Section 1 provides a brief overview of the disclosure system.

• Section 3 provides guidance for conducting reviews.

• Section 4 provides more detailed guidance for reviewing a number of commonly

reported interests and affiliations.

Disclaimer

This guide is intended for use in reviewing executive branch confidential financial

disclosure reports filed on or after January 1, 2019.

Do not rely on statements in this guide for investment advice. This guide is solely for

general informational purposes. This guide supersedes earlier OGE training

publications, but applicable statutes and regulations are the final authorities.

In addition, although the use of the sample language provided in this guide promotes

a degree of consistency in reporting common items, OGE recognizes that there may

be other ways of reporting particular interests.

Superseded

Confidential Financial Disclosure Guide, Section 1 6

Version: 1/2019

Section 1: Confidential Financial Disclosure System

This section provides an overview of the confidential financial disclosure system,

including information on why people file, who files, what forms are used, when forms

are due, what an agency reviewer’s role is, and how long reports are retained.

Purpose

The basic purpose of the confidential financial disclosure system is to assist

employees and their agencies in avoiding conflicts between official duties and

private financial interests or affiliations.

Authority

The Ethics in Government Act of 1978, as amended (the “Act”), requires high-level

federal officials to make public disclosures of selected personal financial interests and

affiliations. Section 107 of the Act and Section 201(d) of Executive Order 12674 (as

modified by E.O. 12731) provide authority for OGE to establish a confidential

financial disclosure system for those executive branch employees who, though not

subject to the public financial disclosure system, have duties that involve a

heightened risk of potential or actual conflicts of interest. The implementing

regulations for the confidential financial disclosure system can be found at 5 C.F.R.

part 2634, subpart I.

Officials Required to File

General Rule

5 C.F.R. § 2634.904(a)(1)

An employee is covered by the confidential financial disclosure system if the

employee’s position meets the following criteria:

1. The employee’s position does not meet the pay or classification thresholds for

public filing.

(Note: This formulation simplifies the rule. More precisely, the regulation

includes each officer or employee in the executive branch whose position is

classified at GS-15 or below of the General Schedule prescribed by 5 U.S.C.

§ 5332, or the rate of basic pay for which is fixed, other than under the General

Schedule, at a rate which is less than 120% of the minimum rate of basic pay for

GS-15 of the General Schedule; each officer or employee of the United States

Postal Service or Postal Regulatory Commission whose basic rate of pay is less

Superseded

Confidential Financial Disclosure Guide, Section 1 7

Version: 1/2019

than 120% of the minimum rate of basic pay for GS-15 of the General Schedule;

each member of a uniformed service whose pay grade is less than 0-7 under

37 U.S.C. § 201; and each officer or employee in any other position determined

by the designated agency ethics official to be of equal classification.)

and

2. The agency has determined that the duties and responsibilities of the employee’s

position require the employee to participate personally and substantially through

decision or the exercise of significant judgment, and without substantial

supervision and review, in taking a Government action regarding:

a. contracting or procurement;

b. administering or monitoring grants, subsidies, licenses, or other federally

conferred financial or operational benefits;

c. regulating or auditing any non-federal entity; or

d. other activities in which the final decision or action will have a direct and

substantial economic effect on the interests of any non-federal entity.

To simplify the application of these criteria, agencies may establish an appropriate

threshold based on the position’s monetary level of procurement authority, pay

grade, or degree of supervision. Agencies should also apply the criteria in

conjunction with their exclusion authority (see below) to ensure that individuals

are not required to file if the possibility of conflict is remote.

Even if the employee’s position does not involve such participation, an agency

may require confidential filing if the agency determines that, based on the

employee’s duties and responsibilities, filing is required in order for the employee

to avoid involvement in a real or apparent conflict of interest. Nevertheless,

agencies should limit such designations to those pay grades where the duties and

responsibilities clearly make filing necessary and relevant. For more help, see

OGE DAEOgram DO-94-031 (September 14, 1994).

Special Government Employees

5 C.F.R. § 2634.904(a)(2)

Special Government employees (SGEs) must file confidential financial disclosure

reports if they meet the criteria outlined above, serve on a Federal Advisory

Committee, or otherwise have a substantial role in the formulation of agency policy.

SGEs need not file if they are required to file public financial disclosure reports or if

they are excluded from filing based on the agency’s determination that the possibility

of conflicts is remote.

Superseded

Confidential Financial Disclosure Guide, Section 1 8

Version: 1/2019

Definition

18 U.S.C. § 202

A special Government employee (SGE) is defined by 18 U.S.C. § 202 to include an

officer or employee who is retained, designated, appointed, or employed by the

Government to perform temporary duties, with or without compensation, for not more

than 130 days during any period of 365 consecutive days. The term also includes a

Reserve officer of the Armed Forces or an officer of the National Guard while on

active duty solely for training, or if serving involuntarily.

At the time of appointment, the appointing official determines whether the employee

will be reasonably expected to work more than 130 days in the 365 days after the

appointment date. If an agency designates an employee as an SGE, based on a good

faith estimate, but the employee unexpectedly serves more than 130 days during the

ensuing 365-day period, the individual still will be deemed an SGE for the remainder

of that period. However, upon the commencement of the next 365-day period, the

agency should reevaluate whether the employee is correctly designated as an SGE,

(i.e., expected to serve no more than 130 days).

Supplemental Reporting Requirements

5 C.F.R. §§ 2634.103 and 2634.904(a)(3)

An individual who files a public financial disclosure report may also be required by

agency supplemental regulations to file an additional confidential financial disclosure

report containing supplemental information. Such regulations must receive prior

written approval from OGE.

Exclusions

5 C.F.R. § 2634.904(b)

Agencies may exclude positions otherwise subject to the filing requirements if the

agency head or designee determines that there is only a remote possibility that the

incumbent will be involved in a real or apparent conflict of interest. Agencies should

document such determinations in writing.

Review of Confidential Filer Status

5 C.F.R. § 2634.906

An employee may request a review of a determination that the employee’s position

meets the criteria requiring confidential financial disclosure. The review is conducted

by the head of the agency or an officer designated by the agency head, and the

decision reached by the agency head or designee is final.

Superseded

Confidential Financial Disclosure Guide, Section 1 9

Version: 1/2019

Types of Reports and Filing Deadlines

New Entrant Reports (excluding special Government employees)

5 C.F.R. §§ 2634.903(b) and 2634.908(b)

Requirement to File

A confidential filer must submit a new entrant report within 30 days of assuming the

duties of a covered position, unless an extension is granted. An agency may require

that a prospective entrant to a covered position file a report before serving in the

position if needed to ensure that there are no insurmountable ethics concerns.

Exceptions to the Filing Requirement

An employee need not file a new entrant report in the following cases:

• The employee assumed the duties of the position within 30 days of leaving a

position that was subject to either public or confidential financial disclosure,

provided that the filer satisfied the applicable filing requirements for the prior

position. The agency at which the new position is located, however, should

obtain a copy of the filer’s most recent report and review that report for any

potential conflicts. In addition, the employee must comply with any supplemental

reporting requirements that apply to the new position.

• The employee filed a report while being considered for the position, though the

agency may request an update if more than 6 months has passed.

• The designated agency ethics official (or designee) does not reasonably expect the

employee to serve in the covered position for more than 60 days in the following

12-month period. If the employee actually serves more than 60 days, the

employee must file a new entrant report within 15 calendar days after the 60th

day. For full-time employees, count the number of consecutive calendar days that

the employee served in the position, including weekends and holidays. For part-

time employees, count only days that the employee actually worked.

Reporting Period

The reporting period for a new entrant report varies according to the Part being

completed.

• Part I: Filers report assets as of the date of filing. Filers report sources of earned

income, honoraria, and other non-investment income for the preceding 12 months.

• Part II: Filers report liabilities as of the date of filing.

• Part III: Filers report positions for the preceding 12 months.

Superseded

Confidential Financial Disclosure Guide, Section 1 10

Version: 1/2019

• Part IV: Filers report agreements and arrangements as of the date of filing.

Newly Designated Positions

In most cases, an agency has already determined whether the duties and

responsibilities of a position require confidential financial disclosure prior to an

employee’s entry into the position. Therefore, the employee files a new entrant report

upon assuming the duties. In certain cases, however, an agency may make this

determination for a position that an employee already occupies. The incumbent

employee in this case would file a new entrant report within 30 days of the agency

designating the position as requiring confidential financial disclosure. See OGE

DAEOgram DA-10-20-92 (October 19, 1992).

Annual Reports (excluding special Government employees)

5 C.F.R. §§ 2634.903(a) and 2634.908(a)

Requirement to File

An employee who served in a covered position for more than 60 days during a

calendar year must file an annual report by February 15 of the following year. If the

15th falls on a weekend or holiday, the due date is the next workday.

For full-time employees, count the number of consecutive calendar days that the

employee served in the position, including weekends and holidays. For part-time

employees, count only days that the employee actually worked.

Exceptions to the Filing Requirement

Agencies need not collect annual reports from an individual who is no longer in a

covered position as of February 15. In addition, special Government employees do

not file annual reports.

Reporting Period

An annual report covers the preceding calendar year. Therefore, a filer submitting a

report by February 15, 2019, must ordinarily include information for the period

January 1, 2018, through December 31, 2018. Filers may exclude information for a

period covered by a prior confidential or public financial disclosure report.

Moving between Covered Positions

If a filer moves between covered positions at different agencies, the individual should

file the next annual report with his or her new agency. The new agency should

provide a copy of the report to the filer’s former agency for review if any of the

interests raise potential conflicts or if the former agency requests a copy. This review

by the former agency is not a full review within the meaning of this guide and no

intermediate or final certification is required.

Superseded

Confidential Financial Disclosure Guide, Section 1 11

Version: 1/2019

Special Government Employees (SGEs)

The confidential financial disclosure requirements for special Government employees

differ from the requirements applicable to other United States Government

employees.

Requirement to File

5 C.F.R. §§ 2634.903(b) and 2634.904(a)(2)

An SGE must file a new entrant report within 30 days of starting a covered position

as an SGE. In addition, an SGE must file a new entrant report each year upon the

individual’s “reappointment or redesignation” as an SGE for a new 365-day period.

Exceptions to the Filing Requirement

An SGE need not complete a report when starting a position as an SGE if either of the

following conditions applies:

• The employee assumed the duties of the position within 30 days of leaving a

position that was subject to public or confidential financial disclosure, provided

that the filer satisfied the applicable filing requirements for that position. The

agency at which the new position is located, however, should obtain a copy of the

filer’s most recent report and review for any potential conflicts.

• The employee filed a report while being considered for the position, though the

agency may request an update if more than 6 months has passed.

The exception for employees who serve 60 days or less in a covered position does not

apply to SGEs.

Due Date Considerations

Notwithstanding the 30-day timeframe, individuals being considered for positions

requiring Presidential appointment and Senate confirmation (PAS) file their reports

pursuant to the special deadlines and procedures that govern the PAS nominee

process. In addition, SGEs appointed to a Federal Advisory Committee Act

committee must file their reports before rendering any advice or in no event later than

the first committee meeting. For all other SGEs, agencies may require the individuals

to file their reports prior to serving if needed to ensure that there are no

insurmountable ethics concerns.

With respect to reappointments and redesignations, an SGE with a multiyear term

would ordinarily file an additional new entrant report each year on the anniversary of

that employee’s appointment date. However, OGE permits agencies to specify one

date each year on which to collect follow-on new entrant reports from all SGEs (or

discrete groups of SGEs, such as all members of a given advisory committee) who

Superseded

Confidential Financial Disclosure Guide, Section 1 12

Version: 1/2019

serve for terms in excess of one year. See OGE DAEOgram DO-95-019

(April 11, 1995) and OGE DAEOgram DO-00-003 (February 15, 2000).

Reporting Period

The same reporting period rules apply to all new entrant reports, including those filed

by SGEs.

Relationship to the Public Filing Requirements

An SGE must file a public financial disclosure report if the SGE serves in a position

that meets the criteria for public filing set out at 5 C.F.R. § 2634.202 and serves in the

position for more than 60 days. An SGE who is expected to serve no more than 60

days would file a confidential financial disclosure report; however, if the SGE

actually exceeds the 60-day threshold, the SGE must file a public report within 15

calendar days following the 60th day of service.

In certain cases, agency ethics officials do not expect an employee to serve more than

60 days but know there is a real possibility that the employee could do so. In such

cases, agency ethics officials may permit, but not require, an employee to file a

modified OGE Form 278e in lieu of a confidential financial disclosure form. The

modified OGE Form 278e would include only the information required by the

confidential financial disclosure requirements. For example, in Parts 2, 5, and 6 of

the OGE Form 278e, the filer would report the assets that meet a reporting threshold

but would not complete the value and income fields. Similarly, the filer would

complete only the Creditor Name and Type fields in Part 8. The modified OGE Form

278e would be treated as confidential and marked “not for public release” (or

“confidential”), unless and until the employee works more than 60 days in that

calendar year. If the employee does work more than 60 days, the employee must

update the report within 15 days of the 60th day, including all of the information

required for a public OGE Form 278e. See OGE DAEOgram DO-03-021 (October

23, 2003) for additional guidance.

Alternatively, an employee may voluntarily complete all of the information required

for a public OGE Form 278e at the time the employee files confidentially. For

example, unlike the procedure discussed above, the employee may complete the value

and income fields for each entry in Parts 2, 5, and 6. The OGE Form 278e would be

treated as confidential and marked “not for public release” (or “confidential”), unless

and until the employee works more than 60 days in that calendar year. In the event

that the employee does serve more than 60 days, the agency could use the existing

confidential OGE Form 278e to satisfy the public reporting requirement, provided

that the information is no more than 6 months old. The agency would simply remove

the confidential designation from the report within 15 days after the 60th day worked.

Superseded

Confidential Financial Disclosure Guide, Section 1 13

Version: 1/2019

“Acting” Capacity

5 C.F.R. § 2634.903

Employees are sometimes assigned to perform the duties of a position in an “acting”

capacity. Such employees are subject to any financial disclosure requirements

applicable to that position.

New Entrant

An employee who acts in a position meeting the criteria for confidential filing must

file a new entrant report. A report, however, is not required if (1) the employee is

already a confidential or public filer or (2) the employee is reasonably expected to

serve no more than 60 days in the position. Employees excluded from filing based on

their expected days of service must file a report if they actually exceed 60 days of

service, and this report is due within 15 days of exceeding the 60-day threshold.

For example, an employee, who otherwise does not file a financial disclosure report,

assumes the duties of a covered position on an acting basis on October 29, 2019. The

employee is not reasonably expected to serve in the position for more than 60 days in

the following 12-month period. No report is required. However, the employee later

does serve more than 60 days. The employee, therefore, must file a new entrant

report within 15 calendar days of exceeding 60 days.

Annual

An employee who acts in a position subject to confidential filing for more than 60

days during a calendar year must file an annual report. A report, however, is not

required if (1) the employee is already a public filer or (2) the employee leaves the

position prior to February 15 of the following year.

For example, an employee, who otherwise does not file a financial disclosure report,

assumes the duties of a covered position on an acting basis on October 29, 2019. The

employee is still performing the duties of the position on February 15, 2020. An

annual report is required. If the employee’s acting service ends prior to

February 15, 2020, no annual report is required.

Details between Federal Agencies

5 C.F.R. § 2634.605(b)(1)

An individual detailed to another agency may be subject to the confidential filing

requirements based on the position at the individual’s home agency, the position at

the agency to which the individual is detailed (detail agency), or both positions. If the

position at the individual’s home agency is subject to confidential financial

disclosure, the individual must continue to file the report with the home agency. The

individual’s home agency would consult with the detail agency, as appropriate, to

determine whether the report discloses any potential conflicts with the duties of the

position to which the individual is detailed. If the individual is only subject to

Superseded

Confidential Financial Disclosure Guide, Section 1 14

Version: 1/2019

confidential financial disclosure based on the position at the detail agency, the

individual would file instead with the detail agency. See OGE DAEOgram DA-10-

20-92 (October 19, 1992).

Intergovernmental Personnel Act Detailees

In December 2001, the Intergovernmental Personnel Act (IPA) was amended to make

individuals who are detailed to federal agencies under the IPA “employees” of the

federal agency for purposes of the Ethics in Government Act. Accordingly, IPA

detailees may be required to file a confidential financial disclosure report if their

duties and responsibilities meet the criteria at 5 C.F.R. § 2634.904(a)(1). See OGE

DAEOgram DO-02-029 (December 9, 2002) and OGE DAEOgram DO-06-031

(October 19, 2006).

Individuals Who Are Not Government Employees

The confidential financial disclosure requirements apply only to individuals who are

current or prospective United States Government employees. Agencies may not use

the OGE Form 450 (Executive Branch Confidential Financial Disclosure Report) to

collect information from other individuals, such as contractors or members of

advisory committees who are appointed to represent outside interests. See OGE

DAEOgram DO-95-043 (December 13, 1995). Note that Intergovernmental

Personnel Act detailees and advisory committee members appointed as special

Government employees are United States Government employees for purposes of the

confidential financial disclosure requirements.

Confidential Financial Disclosure Forms

OGE Form 450

5 C.F.R. § 2634.601(a)(3)

The OGE Form 450 (Executive Branch Confidential Financial Disclosure Report) is

the standard form for making a confidential financial disclosure. A confidential filer

must use the OGE Form 450, unless otherwise authorized to use an alternative form.

OGE Optional Form 450-A

Effective January 1, 2019, the OGE Optional Form 450-A is no longer approved for

use. Agencies that wish to use a similar format as an alternative reporting procedure

can submit a written request to OGE in accordance with 5 C.F.R. § 2634.905.

Superseded

Confidential Financial Disclosure Guide, Section 1 15

Version: 1/2019

Supplemental and Alternative Forms

5 C.F.R. §§ 2634.103, 2634.601(c), and 2634.905

With the prior written approval of OGE, agencies may require employees to file

additional confidential financial disclosure forms that supplement the standard public

or confidential forms. Agencies, with the prior written approval of OGE, may also

choose to use an alternative confidential financial disclosure form and procedure in

lieu of the OGE Form 450.

Extensions

Agency Extensions

5 C.F.R. § 2634.903(d)(1)

Agencies may, for good cause shown, grant any employee or class of employees a

filing extension or several extensions totaling no more than 90 days. Extensions do

not change the reporting period. For example, if a filer was originally required to file

a new entrant report on October 15, 2019, but received a 90-day extension, the end of

the reporting period for the purpose of valuing assets is still October 15, 2019, and the

reporting period for non-investment income is still October 15, 2018, through

October 15, 2019.

OGE recommends that extension requests and approvals be documented in writing.

In addition, the existence of an extension should be noted on a report once filed.

Service in a Combat Zone or Service during a Period of National Emergency

5 C.F.R. § 2634.903(d)(2)

An individual is automatically eligible for an extension if the individual has served in

a combat zone or was required to perform services away from the individual’s

permanent duty station following a declaration by the President of a national

emergency.

This extension runs until 90 days after the later of the following two dates:

• the last day of the individual’s service in the combat zone or away from the

individual’s permanent duty station; or

• the last day of the individual’s hospitalization as a result of an injury received or a

disease contracted while serving during the national emergency.

The terms of this extension differ from those of a similar combat zone extension

available to public filers.

Superseded

Confidential Financial Disclosure Guide, Section 1 16

Version: 1/2019

Filing Penalties

5 C.F.R. §§ 2634.701 and 2634.909

An agency may take any appropriate action, including adverse action, against

employees who have not filed or who have filed a false, incomplete, or late report, in

accordance with applicable personnel laws and regulations. An individual who

knowingly and willfully falsifies a report may also be subject to criminal prosecution.

Agency Procedures

Section 402(d) of the Ethics in Government Act, as amended, requires that each

agency establish written procedures for handling financial disclosure reports filed

with the agency. See OGE DAEOgram DA-09-03-92 (September 3, 1992).

Records Management

Access and Use

5 C.F.R. § 2634.604

Reports filed pursuant to the executive branch confidential financial disclosure

regulation are protected under the Privacy Act. Confidential reports may be used

only for the purposes stated in the Privacy Act Statement, which is included on the

first page of the form.

Retention Schedule

5 C.F.R. § 2634.604

The following discussion summarizes the applicable requirements for confidential

financial disclosure reports. See the OGE/GOVT-2 (Privacy Act) system of records

for additional information. See also General Records Schedule 2.8 (Federal Records

Act).

Reports Filed by Employees Who Served in the Position

Agencies must retain confidential financial disclosure reports (OGE Form 450 and

agency alternative forms) for a period of 6 years from the date of receipt. Agencies

must destroy the report after 6 years, unless the report is needed for an ongoing

investigation or to understand an agency alternative form that makes reference to the

information contained in that report.

Reports Filed by PAS Nominees Who Are Not Confirmed

Individuals file financial disclosure reports when nominated to positions requiring

Presidential appointment and Senate confirmation (PAS). If the individual is

Superseded

Confidential Financial Disclosure Guide, Section 1 17

Version: 1/2019

subsequently confirmed by the Senate, the agency must retain the report for 6 years

from the date of receipt, unless the report is needed for an ongoing investigation or to

understand an agency alternative form that is still within its 6-year retention period.

If the individual is not confirmed, however, the agency retains the report for only 1

year after the nominee ceases to be under consideration for the position, unless the

report is needed for an ongoing investigation.

Reports Filed by Other Prospective Employees Who Do Not Serve in the Position

If a prospective employee, other than a PAS nominee, provides a confidential

financial disclosure report and subsequently does not assume the duties of the

position, the agency would treat the report as a draft rather than as a final, filed report.

Drafts may be destroyed when no longer needed by the agency.

Superseded

Confidential Financial Disclosure Guide, Section 2 18

Version: 1/2019

Section 2: OGE Form 450 – Report Contents

This section explains what information a filer must provide in the cover page and

each substantive Part of the OGE Form 450.

Summary of Contents

The OGE Form 450 consists of one page of instructions, a cover page, five

substantive Parts, and a final page of examples. However, filers need only submit

those pages with reportable information, unless otherwise required by their

agency. For example, a filer with no reportable interests would submit only the

cover page.

Each of the five substantive Parts addresses a different category of interest that

the filer must disclose. The type of report (i.e., new entrant or annual) determines

the reporting period as well as the applicability of the gift and travel

reimbursement reporting requirements.

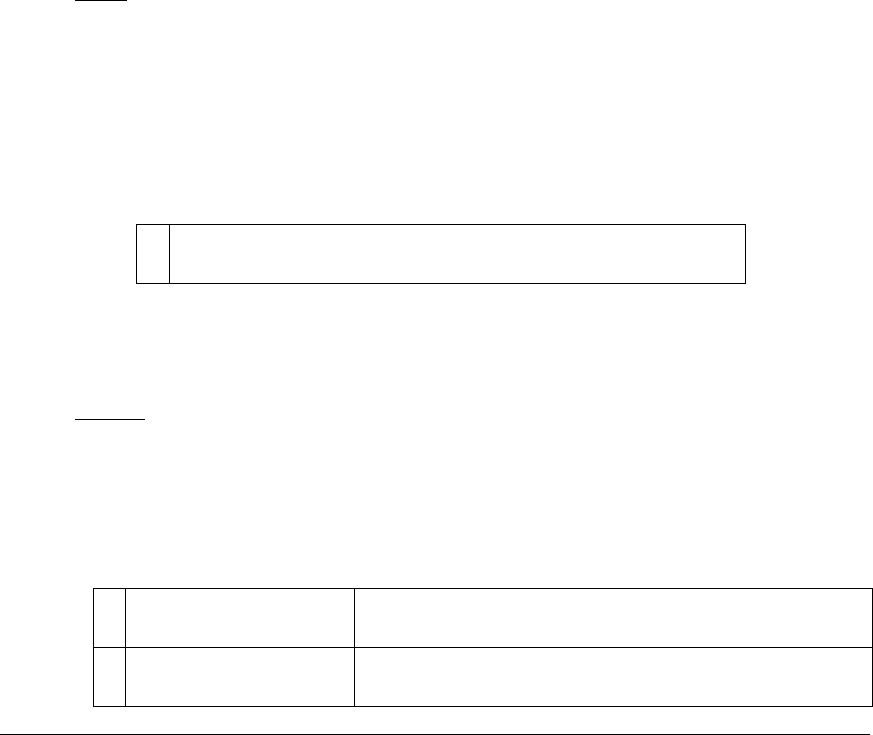

Reporting Periods and Individuals Covered

PART

REPORTING PERIOD

INDIVIDUALS

COVERED

New Entrant

Annual

PART I

Assets and Income

Assets: Date of Filing

Investment Income: N/A

Non-Investment Income:

12 Months Preceding the

Date of Filing

Preceding

Calendar Year*

Filer, Spouse, and

Dependent Children

PART II

Liabilities

Date of Filing

Preceding

Calendar Year*

Filer, Spouse, and

Dependent Children

PART III

Outside Positions

12 Months Preceding the

Date of Filing

Preceding

Calendar Year*

Filer Only

PART IV

Agreements or

Arrangements

Date of Filing

Preceding

Calendar Year*

Filer Only

PART V

Gifts and Travel

Reimbursements

N/A

Preceding

Calendar Year*

Filer, Spouse, and

Dependent Children

* Filers may exclude information for a period covered by a prior confidential or public

financial disclosure report.

Superseded

Confidential Financial Disclosure Guide, Section 2 19

Version: 1/2019

Spouses and Dependent Children

Scope of Reporting Requirements

General Rule

5 C.F.R. §§ 2634.907(a) and (h)

Filers need to report the interests of spouses and dependent children in several

Parts of the OGE Form 450, but the reporting thresholds and requirements may

differ, depending on the type of interest. The requirements are explained in the

instructions for each type of reportable interest.

Definitions

Spouse

For purposes of financial disclosure and other federal ethics rules, “spouse”

means an individual to whom the filer has been legally married, regardless of the

filer’s state of residence. The term “spouse” does not include an individual with

whom the filer is in a civil union, domestic partnership, or other relationship other

than marriage. See OGE Legal Advisory LA-13-10 (August 19, 2013).

Dependent Child v. Minor Child

The basic criminal conflict of interest statute (18 U.S.C. § 208) uses the term

“minor child,” but the financial disclosure requirements (and the Standards of

Conduct provisions on impartiality) refer more broadly to “dependent children.”

For purposes of financial disclosure, “dependent child” means an individual who

is:

1. a son, daughter, stepson, or stepdaughter of the filer; and

2. unmarried, under age 21, and living in the filer’s household or considered a

dependent by tax code standards.

“Minor child” is a class of children defined by state law, usually as under age 18.

Tests for Separateness

5 C.F.R. § 2634.907(h)(6)

A filer need not report assets, investment income, or liabilities of a spouse or

dependent child if the interests strictly meet all the tests for separateness in the

regulation. These tests, however, are very rarely met. For example, an asset that

is reported on a joint tax return or held in a trust for a child’s education is a

benefit to the filer. Thus, the asset should be reported. A practical effect of these

Superseded

Confidential Financial Disclosure Guide, Section 2 20

Version: 1/2019

tests is that filers who complete joint tax returns, cohabitate, share expenses, or

have not been disinherited by their spouses must report the spouse’s interests.

Changes in Status during a Reporting Period

Marriage during a Reporting Period

When a filer gets married during the reporting period, the filer reports:

• In Part I: A spouse’s assets and sources of income that met an applicable

reporting threshold after the date of the marriage.

• In Part II: A spouse’s liabilities that met the applicable reporting threshold

after the date of the marriage.

• In Part V (annual filers only): A spouse’s gifts and travel reimbursements that

were received after the date of the marriage.

Divorce or Separation

5 C.F.R. § 2634.907(h)(5)

A filer who is divorced or permanently separated need not report a spouse’s

interests for the period before or after the divorce or permanent separation.

However, note that even in situations where there is no reporting requirement,

18 U.S.C. § 208 will still apply to particular matters in which an employee knows

his or her separated spouse has a financial interest.

No Longer a Dependent

The filer need not report the sole interests of any child who was not a dependent

as of the date of filing. The filer, however, must still report any interests that are

(or were) also those of the filer or the filer’s spouse (e.g., a child’s loan for which

the filer co-signed).

Distinguishing a Filer’s Entries from the Entries of a Spouse or Dependent Child

Entries for the assets, income, and liabilities of spouses and dependent children

may be marked “S” or “DC” (or “J” for joint) if the filer wishes to distinguish

them from the filer’s own assets, income, and liabilities. These designations are

not required but are often helpful.

Superseded

Confidential Financial Disclosure Guide, Section 2 21

Version: 1/2019

Use of Brokerage Statements and Attachments

5 C.F.R. § 2634.907(j)(2)

Agencies may permit a filer to attach brokerage statements, bank statements,

personal spreadsheets, and other financial materials in lieu of entering the

information directly in the OGE Form 450. However, an agency may permit such

materials only if they readily present, in a clear and concise fashion, all of the

information that the filer would have been required to enter in the OGE Form 450.

Because brokerage statements and other financial reports exist in many formats,

OGE cannot provide guidelines that will cover every situation. Nonetheless, an

(1) clearly identify the assets by name; (2) provide a sufficient description of an

asset when required for that asset type; and (3) clearly indicate which assets are

still held.

Filers are responsible for ensuring that they observe the limitations on using

attachments in lieu of data entries in the OGE Form 450 and that they redact

sensitive information not required by the confidential financial disclosure

regulation, such as account numbers and home addresses. Agencies, however,

should provide guidance to filers regarding the rules applicable to the use of

attachments, and agency reviewers need to evaluate the appropriateness of any

attachments as part of the review process. If an attachment proves insufficient, a

reviewer should request follow-up information or require that the filer provide a

revised attachment or enter the information in the OGE Form 450.

Special rules apply for individuals who file nominee reports in connection with a

position that requires Presidential appointment and Senate confirmation (PAS).

PAS nominee filers may not attach brokerage statements in lieu of completing the

OGE Form 450. In certain circumstances, OGE may permit a nominee filer to

provide clarifying notes in an attachment to the OGE Form 450.

Cover Page

Purpose

The cover page serves four basic functions. First, it provides relevant background

information about the filer. Second, it indicates whether the report was filed in a

timely manner. Third, it includes reporting statements that permit the filer to

exclude any unneeded subsequent pages. Fourth, it collects the signatures of the

filer and the reviewer(s).

Superseded

Confidential Financial Disclosure Guide, Section 2 22

Version: 1/2019

Field Instructions

(1) Date Received by Agency: The agency, not the filer, completes this required

field.

(2) Page Number: A page number should be included on each page of the report.

This information will help ensure that the pages remain in sequence.

(3) Employee’s Name: The filer’s name is a required field.

(4) E-mail Address: Agencies should have an e-mail address at which they can

reach the filer. If the information is otherwise readily available, follow-up is not

required.

(5) Position/Title: The report must specify the position for which the individual is

filing. If the filer has not provided this information, the reviewer should make the

appropriate annotation.

(6) Grade: The filer should enter his or her current grade level in the position. If

the filer has not yet entered the position, the filer should enter the anticipated

grade. If the position will not have an assigned grade level, the filer may leave

this field blank; however, the reviewer should confirm that the individual is

required to file.

(7) Agency: The report must specify the agency in which the position is located.

If the filer has a different home agency, the filer should include that information

as well.

1

2

3

4

5

6

7

8

9

10

11

12

13

Superseded

Confidential Financial Disclosure Guide, Section 2 23

Version: 1/2019

(8) Branch/Unit and Address: The report should specify the organizational

component within the agency where the position resides and should include an

office address. If the office address is otherwise readily available, follow-up is

not required.

(9) Work Phone: Agencies should have a work telephone number at which they

can reach the filer if questions arise about the report. If the information is

otherwise readily available, follow-up is not required.

(10) Reporting Status: The type of report must be indicated. If the filer has not

marked the appropriate box, the reviewer should verify that the filer understood

which Parts were required and the applicable reporting periods.

(11) If New Entrant, Date of Appointment to Position: A new entrant filer must

indicate when he or she entered on duty in the current position so that the

reviewer can determine whether the report was filed on time. An annual filer may

leave this box blank. If the filer did not provide this information, the reviewer

should annotate the report.

(12) Check box if Special Government Employee: The report must specify

whether the filer is a special Government employee (SGE). Reviewers should

correct this field if the filer improperly checked (or failed to check) the box.

(13) If an SGE, Mailing Address: Agencies should have a mailing address at

which to contact an SGE filer. If the information is otherwise readily available,

follow-up is not required.

(14) Reporting Statements: The filer must answer “Yes” or “No” to each of the

reporting statements that apply. A new entrant filer completes the statements for

14

15

Superseded

Confidential Financial Disclosure Guide, Section 2 24

Version: 1/2019

Parts I through IV. An annual filer completes all five statements. If the filer

answers “No” to all of the statements, the filer need not include the remaining

blank pages of the report.

(15) Signature of Employee: The filer must sign and date the report certifying

that the statements made are true, complete, and correct to the best of the filer’s

knowledge.

(16) Signature and Title of Supervisor/Other Intermediate Reviewer: These

blocks are provided for agencies that require an intermediate review of the report

prior to examination by the agency’s final reviewing official.

(17) Signature and Title of Agency’s Final Reviewing Official: The agency’s

final reviewing official must sign and date the report to certify that it meets the

requirements set forth in paragraph (b)(2) of 5 C.F.R. § 2634.605. See Section 3

of this guide for additional information.

(18) Comments of Reviewing Officials: Reviewers should use this block to

record any exceptions to the certification statement that they made by signing in

block 16 or 17. They may also use this block to record supplementary

information obtained from the filer. Additionally, reviewers should note in this

block any extensions of the due date granted by the agency.

Part I: Assets and Income

What to Report

5 C.F.R. §§ 2634.907(b), (c), (h)(1), and (h)(2) and 2634.908

A new entrant filer must report the following:

• any asset of the filer, the filer’s spouse, or the filer’s dependent children that

had a value greater than $1,000 as of the date of filing;

16

17

18

Superseded

Confidential Financial Disclosure Guide, Section 2 25

Version: 1/2019

• any source from which the filer received more than $1,000 in earned income,

honoraria, and other non-investment income during the preceding 12 months;

and

• any source from which the filer’s spouse received more than $1,000 in earned

income and honoraria during the preceding 12 months.

An annual filer must report the following:

• any asset of the filer, the filer’s spouse, or the filer’s dependent children that

had a value greater than $1,000 at the end of the preceding calendar year;

• any asset from which the filer, the filer’s spouse, or the filer’s dependent

children received more than $1,000 in income during the preceding calendar

year;

• any source from which the filer received more than $1,000 in earned income,

honoraria, or other non-investment income during the preceding calendar

year; and

• any source from which the filer’s spouse received more than $1,000 in earned

income and honoraria during the preceding calendar year.

Note: Sources of earned income for dependent children need not be reported

because it has been determined that the utility of such information in assessing

potential conflicts does not outweigh the reporting burden. Nonetheless, filers

should be aware that such sources may pose potential conflict or appearance

concerns if the filer can participate in United States Government actions affecting

or involving those sources.

How to Report

In general, a filer must provide a description that is sufficient for the reviewer to

identify the asset or source of income for purposes of the conflict of interest

analysis. The amount of detail required will vary by the type of asset or income.

• Stock and other equity in a business: Filers must provide the full name of any

reportable businesses and securities. For a privately held business, filers

should describe the line of business as well, unless the filer has already

provided this information in another entry or the reviewer can readily identify

the business (e.g., the business has a web site that provides this information).

Ticker symbols for publicly traded companies are helpful but not required.

• Other assets with specific names (e.g., bonds and mutual funds): Filers must

provide the full name of the asset (e.g., “Fidelity Select Pharmaceuticals” not

just “Fidelity”) and, unless clear from the name, describe the type of asset.

Superseded

Confidential Financial Disclosure Guide, Section 2 26

Version: 1/2019

• Assets without specific names: Filers must describe the type of asset,

including the city and state (or county and state) for real estate.

• Sources of earned or other non-investment income: Filers must provide the

name of any reportable source of earned or other non-investment income and

indicate the type of income. For income related to employment, filers may

ordinarily just note that the source is an employer; however, the reviewer may

need to gather additional information as to the specific types of income if

relevant for the conflict of interest analysis. For a privately held business,

filers should describe the line of business as well, unless the filer has already

provided this information in another entry or the reviewer can readily identify

the business (e.g., the business has a web site that provides this information).

Filers should mark the “No Longer Held” box for (1) assets that were no longer

no longer providing income at the end of the reporting period.

Optional Designation of Ownership

A filer may choose to distinguish among entries belonging to different family

members. For example, the filer may note next to entries (S) for “spouse,” (DC)

for “dependent child,” or (J) for “jointly held.” These designations are not

required but are often helpful.

Reporting Standards for PAS Nominees

Filers who are completing reports as nominees to positions requiring Presidential

appointment and Senate confirmation (PAS) face a heightened level of scrutiny.

As part of the review process, such filers may be asked to provide more detailed

descriptions of assets and sources of income than would other filers.

Exceptions from the Reporting Requirements

5 C.F.R. § 2634.907(c)(3)

Filers do not report the following:

• salaries or retirement benefits from United States Government employment

(including Thrift Savings Plan accounts);

• income from Social Security, veterans’ benefits, and other similar

United States Government benefits;

• certificates of deposit (CDs), savings accounts, and checking accounts with

banks, credit unions, and similar depository institutions;

• money market mutual funds and money market accounts;

Superseded

Confidential Financial Disclosure Guide, Section 2 27

Version: 1/2019

• diversified mutual funds or unit investment trusts, including exchange-traded

funds that qualify for the exemption at 5 C.F.R. § 2640.201(a);

• diversified funds in an employee benefit plan that qualify for the exemption at

5 C.F.R. § 2640.201(c)(1)(ii) or 5 C.F.R. § 2640.201(c)(1)(iii);

• term life insurance;

• a personal residence, unless rented out during the reporting period;

• United States Government obligations, including U.S. Treasury bonds, bills,

notes, and savings bonds;

• Government securities issued by United States Government agencies; and

• a personal liability owed to the filer, spouse, or dependent child by a spouse,

parent, sibling, or child.

In addition, a filer need not report the assets of a former spouse or a spouse from

whom the filer is permanently separated; the assets of a spouse living separate and

apart from the filer with the intention of terminating the marriage or providing for

permanent separation; the assets of a spouse or dependent child that meet the tests

of separateness; and income arising from the dissolution of the filer’s marriage or

permanent separation, such as child support or alimony. See the discussion under

“Spouses and Dependent Children” for more information.

Definition of “personal residence”: A “personal residence” is defined at 5 C.F.R.

§ 2634.105(l) to mean any property used exclusively as a private dwelling by the

filer or the filer’s spouse, which is not rented out during any portion of the

reporting period. Filers may have more than one property that qualifies as a

personal residence (e.g., a vacation home).

Definitions of Asset and the Types of Income

Asset

“Asset” refers to an interest in property held in a trade or business or held for

investment or the production of income. Examples of reportable property

interests (or “assets”) include, but are not limited to, stocks, bonds, investment

funds, and other securities; real estate; retirement interests (e.g., defined benefit or

defined contribution plan); fixed or variable annuities; whole, universal, and

variable life insurance; beneficial interests in trusts and estates; collectible items

for resale or investment; commercial crops; accounts or other funds receivable;

and capital accounts or other asset ownership in a business.

Superseded

Confidential Financial Disclosure Guide, Section 2 28

Version: 1/2019

Investment Income

“Investment income” refers to interest, rents, royalties, dividends, realized capital

gains, and other income derived from an asset. Examples of investment income

include, but are not limited to, income derived from: stocks, bonds, investment

funds, and other securities; real estate; retirement investment accounts; annuities;

the investment portion of life insurance contracts; interests in trusts and estates;

collectible items; commercial crops; accounts or other funds receivable; and

businesses.

Earned Income

“Earned income” includes fees, salaries, commissions, honoraria, and any other

compensation received for personal services but excludes salary from United

States Government employment and other federal benefits, including retirement

and veterans’ benefits. If personal services provided by the filer or the filer’s

spouse or dependent children are a material factor in the production of income

from an asset or business, the income is considered “earned income” for purposes

of financial disclosure rather than “investment income.” A dependent child’s

earned income is not reportable.

Other Non-Investment Income

A remainder category exists for income that is neither investment income nor

earned income. Examples include prizes, scholarships, awards, and gambling

winnings. Filers report only their own sources of other non-investment income.

Other non-investment income received by a spouse or dependent child is not

reportable.

Valuing Assets

5 C.F.R. § 2634.301(e)

Valuation Methods

Filers typically should value a publicly traded security based on its exchange

value. In other cases, filers should use some recognized indication of value for

the type of asset, such as:

• a recent purchase price;

• a recent appraisal;

• the market value of the property as assessed for tax purposes;

• the book value of non-publicly traded stock;

Superseded

Confidential Financial Disclosure Guide, Section 2 29

Version: 1/2019

• the face value of bonds or comparable securities;

• the net worth of a business partnership; or

• the equity value of an individually owned business.

A good faith estimate of the fair market value may be made in any case in which

the exact value cannot be obtained without undue hardship or expense.

Aggregation

When determining whether an asset meets the reporting threshold, a filer must

aggregate the value of the filer’s own holdings with that of the filer’s spouse and

dependent children. Even if the filer chooses to report his or her interest in the

asset on a separate line from the interest of a spouse or dependent child, this

choice does not affect the reporting threshold.

Receipt of Income

General Rule

A filer has received income when the filer has the right to exercise control over

the income, regardless of whether the filer has taken actual possession.

Generally, this means income would be “received” for purposes of financial

disclosure when received for purposes of federal income tax. Note, however, that

income would be reportable on a financial disclosure report even if exempt from

federal income tax (e.g., interest on municipal bonds). In other words, a filer’s

financial disclosure report generally will correspond to the filer’s taxable income

in terms of when it is counted but not necessarily what is counted.

Example 1: A filer has received dividends on a stock held even if the dividends

are reinvested.

Example 2: A filer has received a payment for services that has been delivered in

the form of a check even though the filer has not cashed the check. Similarly, a

filer who defers collecting a check would still have received the payment for

purposes of financial disclosure. Filers cannot avoid reporting income by

deferring possession of income made available to them.

Aggregation – Filers, Spouses, and Dependent Children

When determining whether income from an asset meets the reporting threshold, a

filer must aggregate income received by the filer, the filer’s spouse, and the filer’s

dependent children.

Superseded

Confidential Financial Disclosure Guide, Section 2 30

Version: 1/2019

Aggregation – Different Types of Income and Losses from a Particular Source

When determining whether income from an asset meets the reporting threshold,

filers must generally use gross income, and filers must aggregate all types of

income received. Capital losses may be subtracted from any gains and other

investment income when calculating the gross amount of investment income

received.

Example 1: A filer received $750 in dividends and $750 in capital gains from an

asset. The total income of $1,500 meets the income reporting threshold. If the

asset instead produced $750 in dividends but was sold at a loss of $500, the total

income of $250 falls below the income reporting threshold.

Example 2: A filer owns a rental property from which the filer received $9,000 in

rent during the reporting period. The filer may not subtract the expenses of

maintaining the property when determining whether the amount of income

received exceeded $1,000.

Income from Partnership, LLCs, and S-Corporations

Filers may use net distributive share, rather than gross income, when determining

the total amount of income received from any partnerships, limited liability

companies, or S-corporations in which the filer has an interest. However, the

filer’s net distributive share has been received for purposes of financial disclosure,

regardless of whether the filer has taken a distribution.

Example: A filer operates a business that is structured as a limited liability

company. The filer must report income from the business even if all of its profit

during the reporting period was reinvested into the business.

Special Treatment of Tax-Deferred Plans and Accounts

OGE does not treat tax-deferred income accruing within a retirement plan or

account as having been received because of the limitations on withdrawal and

other regulatory requirements governing such plans and accounts. The filer,

however, would report distributions as having been received. When determining

whether a distribution meets the reporting threshold, the filer may subtract any

portion that constitutes an investment into the plan or account of previously

received income. In most cases, though, filers will find it easiest to use the total

amount of a distribution during the reporting period.

Example: A filer would not report dividends on a stock as having been received

if the stock is held within an individual retirement account. The filer, however,

would report distributions from the retirement account as having been received.

Superseded

Confidential Financial Disclosure Guide, Section 2 31

Version: 1/2019

Treatment of Underlying Assets

General Rule

5 C.F.R. § 2634.907(c), Note to paragraphs (c)(1) and (c)(2)

Filers frequently report interests in brokerage accounts, managed accounts,

retirement plan accounts, mutual funds, trusts, and other entities through which

the filer has an interest in other assets. These other assets are the “underlying

assets” or “underlying holdings” of the account, fund, trust, or other entity. For

example, a filer may have a brokerage account. Through this account, the filer

might hold interests in various stocks. These stocks are the underlying assets of

the brokerage account. Similarly, a filer may invest in a mutual fund, which, in

turn, invests in stocks and bonds. These stocks and bonds are the underlying

assets of the mutual fund.

As a general rule, filers must report each underlying asset for which the filer’s

interest (aggregated with that of the filer’s spouse and dependent children)

individually meets the reporting requirements.

Example: A filer has a brokerage account with three underlying assets: (1) shares

of ABC Corporation stock valued at $2,000; (2) a bond issued by XYZ, Inc.,

valued at $500; and (3) U.S. Treasury bonds valued at $5,000. None of the assets

produced more than $1,000 in income. The filer must report the ABC

Corporation stock because the value of the stock exceeds the $1,000 reporting

threshold for value. The filer does not have to report the bond issued by XYZ,

Inc., because the bond meets neither the $1,000 reporting threshold for value nor

the $1,000 reporting threshold for income. The U.S. Treasury bonds exceed the

value threshold; however, U.S. Treasury securities are excepted from reporting

per 5 C.F.R. § 2634.907(c)(3).

General Rule Applied to Proportionate Interests

For purposes of valuing an underlying asset in a trust, fund, or other pooled

investment vehicle, filers may use the value of the proportionate interest that the

filer, the filer’s spouse, and the filer’s dependent children have in the underlying

asset. For purposes of measuring income from an underlying asset, filers may use

the amount of income received from that underlying asset attributable to the filer,

the filer’s spouse, and the filer’s dependent children. A filer would need to use

the total value and income of the underlying assets if the filer is unable to

determine whether the proportionate interest in value and income meets a

reporting threshold.

Example: A filer, who is completing an annual report, has a 25% interest in a

family investment fund. The fund had an overall value of $77,000 at the end of

the calendar year and held the following underlying assets: (1) shares of ABC

Corporation stock that had a value of $75,000 and produced $3,000 in dividends

and (2) bonds issued by XYZ, Inc., that had a value of $2,000 and produced

Superseded

Confidential Financial Disclosure Guide, Section 2 32

Version: 1/2019

$5,000 in interest and capital gains. The filer must report the family investment

fund because the filer’s interest in the overall fund exceeded the reporting

thresholds. With respect to the underlying assets of the fund, the filer would

report the ABC Corporation stock because the filer’s proportionate interest in the

ABC Corporation stock had a value that exceeded $1,000 ($75,000 x 25% >

$1,000). In addition, the filer would report the XYZ, Inc., bonds because the

filer’s proportionate interest in the income from the XYZ, Inc., bonds exceeded

$1,000 ($5,000 x 25% > $1,000).

Reduced Disclosure Requirements for Certain Trusts and Funds

5 C.F.R. § 2634.907(i)

A filer need not follow the process outlined above for (1) investment funds that

meet the criteria for “excepted investment funds”; (2) trusts that meet the criteria

for “excepted trusts”; or (3) trusts certified by OGE as part of the qualified trust

program. Excepted trusts and qualified trusts are relatively rare (see the

regulation for additional information), but excepted investment funds are fairly

common.

An excepted investment fund (EIF) is an investment fund that is:

1. independently managed; and

2. widely held; and

3. either publicly traded or available or widely diversified.